“Slow and steady wins the race.” - Aesop

In Canada’s financial sector, that adage is proving true. Insurance is emerging as the tortoise overtaking the hare of fintech and banking.

Fintech startups still dominate the headlines and banks continue to pour billions into digital projects, yet insurance, long dismissed as too slow to innovate, is delivering some of the most compelling growth stories in financial services.

This shift is less about flash and more about fundamentals, with some insurance verticals now growing at a pace that rivals fintech’s best performers.

Warranties, often viewed as insurance’s smaller cousin, are also undergoing a transformation. According to Allied Market Research, Canada’s embedded protection market was valued at $7.85 billion in 2021 and is forecast to reach $22.27 billion by 2031, growing at a strong 11.3% CAGR (2022–2031). What was once an afterthought is now becoming a meaningful growth driver.

And when you dig into the numbers, the real insight is not in the totals but in how different verticals are moving in very different directions.

The story ahead explores why insurance and warranty are emerging as overlooked engines of Canada’s BFSI growth, what is driving health, life, property, and warranty markets, and how this “quiet sector” may ultimately shape the future of financial services more than banks or Fintech.

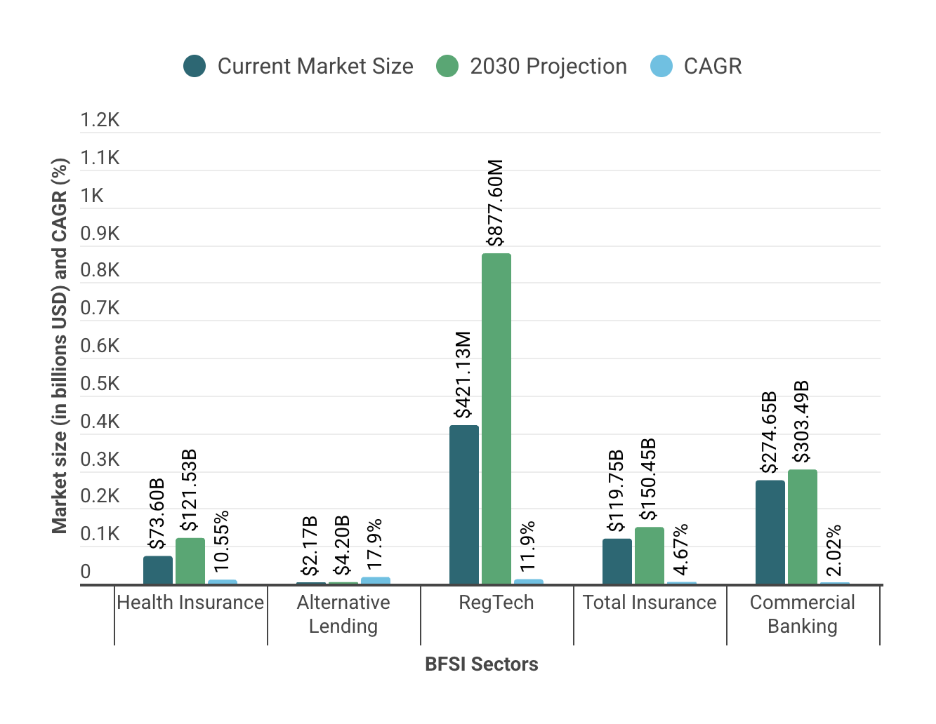

Canada’s insurance market is projected to grow from $119.75 billion in 2025 to $150.45 billion by 2030, representing a steady 4.67% compound annual growth rate (CAGR).

On its own, that may sound modest, but it is already outpacing commercial banking, where the Big Six, despite controlling 93% of deposits, face structural growth limits and deliver only 2.02% growth even though they spend $7.41 billion a year on technology.

Fintech, meanwhile, continues to attract investor enthusiasm. In 2024 alone, the sector raised $9.5 billion in new capital, a 764% year-over-year jump.

Impressive, yes - though part of that growth is linked to investment cycles rather than underlying fundamentals

Insurance, by contrast, is expanding on more stable foundations: demographics, regulatory expansion, and practical innovation that compounds steadily over time.

Let’s break down the numbers with a side-by-side view of how BFSI sectors are projected to grow between 2024 and 2030.

Sources: Mordor Intelligence, Research and Markets, KPMG Canada, Spherical Insights

While fintech often dominates headlines with bold funding rounds and rapid user growth, Insurtech is proving that steady, practical innovation can reshape the industry just as effectively. For example:

Together, these examples highlight an industry innovating in ways that are practical, sustainable, and less dependent on speculation.

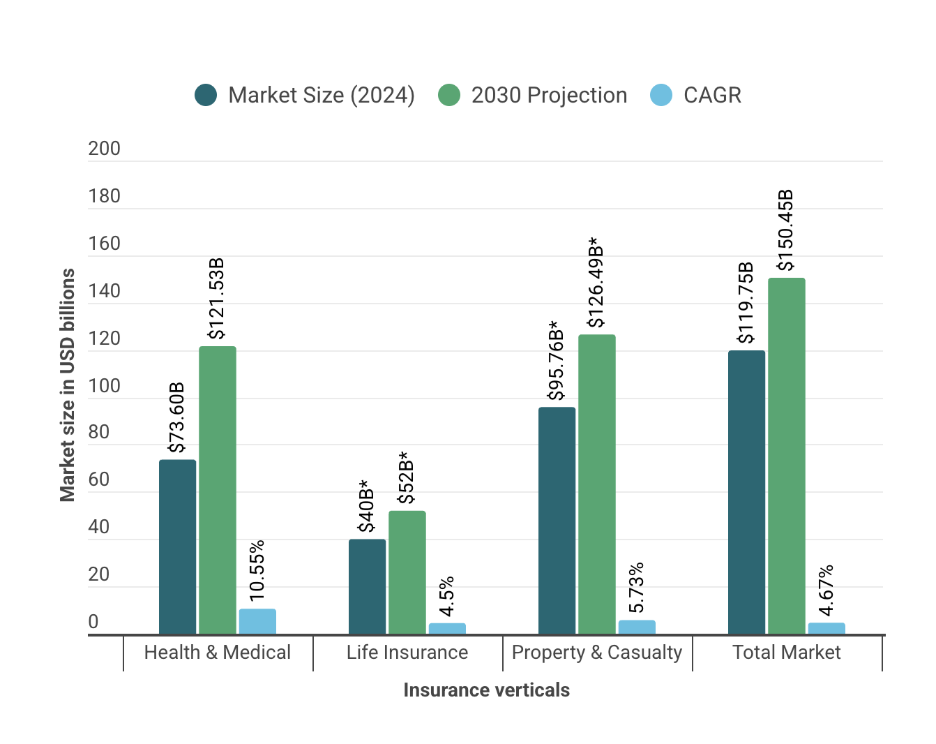

Health insurance is Canada’s fastest-growing major insurance vertical, projected to expand from $73.6 billion in 2025 to $121.5 billion by 2030. That’s a 10.55% CAGR, outpacing most other insurance categories and even rivaling fintech’s hottest growth rates but on a much larger base.

Roughly two-thirds of Canadians (67%) already carry supplementary health insurance, giving the market a strong foundation. Policy shifts are adding more momentum. The Canadian Dental Care Plan, for example- extended coverage to 9 million previously uninsured citizens, creating a new market segment almost overnight.

Demographics are fueling steady growth. As Canada’s population ages, the demand for healthcare services keeps rising, and employers are competing with stronger benefits packages.

Unlike fintech, where growth can swing with speculation, health insurance is expanding on demographic trends that are steady and predictable.

Here’s how health compares with other insurance verticals:

*Estimated based on market share data; *Sources: Mordor Intelligence, Investment Executive, Canadian Underwriter

Health insurance innovation is centered on digital delivery and broader coverage, not just cutting costs. This makes growth more sustainable than fintech’s race-to-zero pricing.

Property and casualty (P&C) insurance is facing the sector’s toughest headwinds. Catastrophic losses hit $8.5 billion in 2024, the highest on record. Climate change is no longer a future risk, and it is a present expense line that continues to erode profitability.

Intact Financial, one of the largest P&C players is targeting 25–30% market share through acquisitions. But while consolidation helps with scale, it doesn’t solve the bigger issue: when natural disasters keep getting more severe, market share gains offer limited protection.

The risk is not theoretical. California offers a cautionary case of how climate pressures are destabilizing markets- State Farm announced it would not renew about 72,000 home insurance policies in 2024, while Allstate had already paused issuing new home insurance coverage.

The California Department of Insurance has imposed moratoriums on non-renewals in wildfire zones, but the underlying crisis remains.

The top five P&C companies control about 50% of the market, a level of concentration that should support innovation. Yet climate pressures mean most strategies remain defensive, focused on shoring up risk rather than chasing growth.

Innovation in P&C is happening, but it is largely about mitigating risk rather than expanding the market. Examples include:

These tools may improve efficiency, but they cannot change the fundamental challenge: insuring assets in an environment where the risks are becoming larger, costlier, and more frequent.

Life insurance is the most concentrated corner of Canada’s insurance market. Just four companies control more than 74.2% of market share:

At first glance, that level of dominance looks similar to banking’s Big Six. But in life insurance, concentration has different implications.

Despite tight control, the business is thriving. In 2023, Canadian life and health insurers paid out a record $128 billion in benefits, proof of strong volume and steady demand.

Where banking’s concentration tends to cap growth by limiting new entrants, life insurance benefits from it: efficient distribution meets steady demographic expansion.

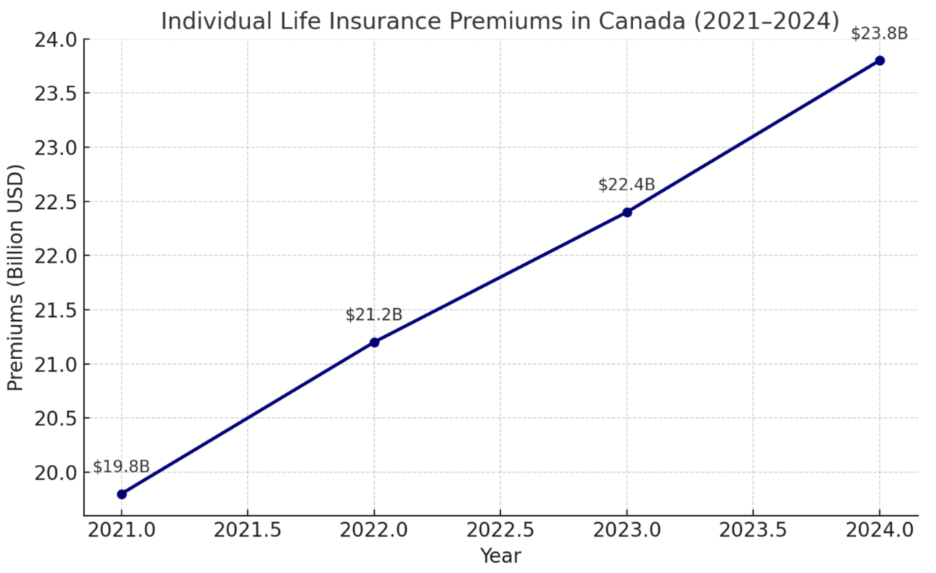

According to CLHIA, total life insurance premiums reached $28.7B in 2023, with 83% ($23.8B) from individual policies and 17% ($4.9B) from group plans. Individual premiums have risen steadily, climbing from about $19.8B in 2021 to an estimated $23.8B in 2024, a CAGR of roughly 6.3%.

Source: CLHIA, Canadian Life & Health Insurance Facts 2023; Investment Executive (2023); CAGR calculations based on CLHIA factbooks.

Innovation is more about improvement than disruption. AI-powered underwriting is already changing the sector:

The result is predictable growth of 5.3% a year. It may not yet be grabbing headlines, but it shows how life insurance is compounding steadily through demographics and gradual innovation.

Extended warranties are quickly becoming insurance’s most innovative growth frontier. In Canada, the extended warranty market is projected to reach $22.27 billion by 2031, growing at an 11.3% CAGR. Merchants typically see average order values rise by up to 14%, and warranty attachment rates average 20.3%, showing that protection plans are already a meaningful part of retail sales.

Here’s why the model works:

A good example comes from SureBright’s merchant network. In the competitive e-bike industry, where thin margins and complex products make differentiation tough, retailers using embedded protection see measurable gains.

By offering extended and accidental warranties at checkout, these merchants achieved:

The lesson is clear: warranties aren’t just a safety net for shoppers - they’re becoming a growth lever for retailers competing in crowded markets

In Canada, warranties also benefit from:

This stability matters. Property insurers are squeezed by climate-related losses. Fintech players face shifting regulations. Warranties, by contrast, operate in a well-defined and predictable framework: one where attach rates, margins, and customer behavior are measurable and repeatable.

That’s the real shift: what used to be a small add-on is now a mainstream growth engine, offering insurers and retailers something rare in financial services a stable and scalable path to revenue.

Insurtech funding is showing steady confidence, not speculation. In 2024, global investment hit $4.2 billion, with Canadian companies playing a meaningful role in that growth.

Let’s see how investment compares across BFSI verticals:

Source: KPMG Canada, Wealth Professional

Another sign of measured growth: 57% of insurers cite AI as a top priority for the next three years. This isn’t about chasing hype. It points to systematic investment in efficiency and risk management.

The takeaway is clear: Insurtech is attracting capital, but the focus is on sustainability and operational improvements, not short-term speculation.

Insurance has several strengths that make its growth story more durable than many other BFSI verticals:

Taken together, these advantages explain why insurance may grow more steadily and prove more resilient than other financial sectors.

One reason growth patterns diverge across Canada’s financial sector is market concentration. The more concentrated a sector is, the harder it is for new entrants to expand the market - while fragmented sectors leave more room for innovation.

Sources: Wiley Online Library, NerdWallet Canada, Mordor Intelligence

Banking: Extreme concentration (93% deposits with the Big Six) limits market expansion, even with heavy technology investment.

Insurance: Mixed concentration means growth varies.

Insurance and warranty growth may prove more sustainable than fintech’s spectacular but often fragile trajectories. Health insurance’s 10.55% CAGR is built on demographic certainty rather than venture capital cycles.

Open banking, expected in 2026, could reshape competition across BFSI. Yet insurance companies hold advantages that banks and FinTech's may find harder to replicate the long-standing customer relationships and access to valuable data that create more defensible positions.

The warranty industry’s embedded model also avoids many of the pitfalls facing traditional insurance. As products become more complex and expensive, attaching coverage at the point of sale generates revenue that scales with the economy rather than competing against it.

Canada’s BFSI growth story isn’t about sweeping disruption. It is about sector-by-sector evolution, where insurance and warranty providers show that steady innovation can outlast flashy speculation.

Or, to borrow from Aesop - sometimes the tortoise really does beat the hare.